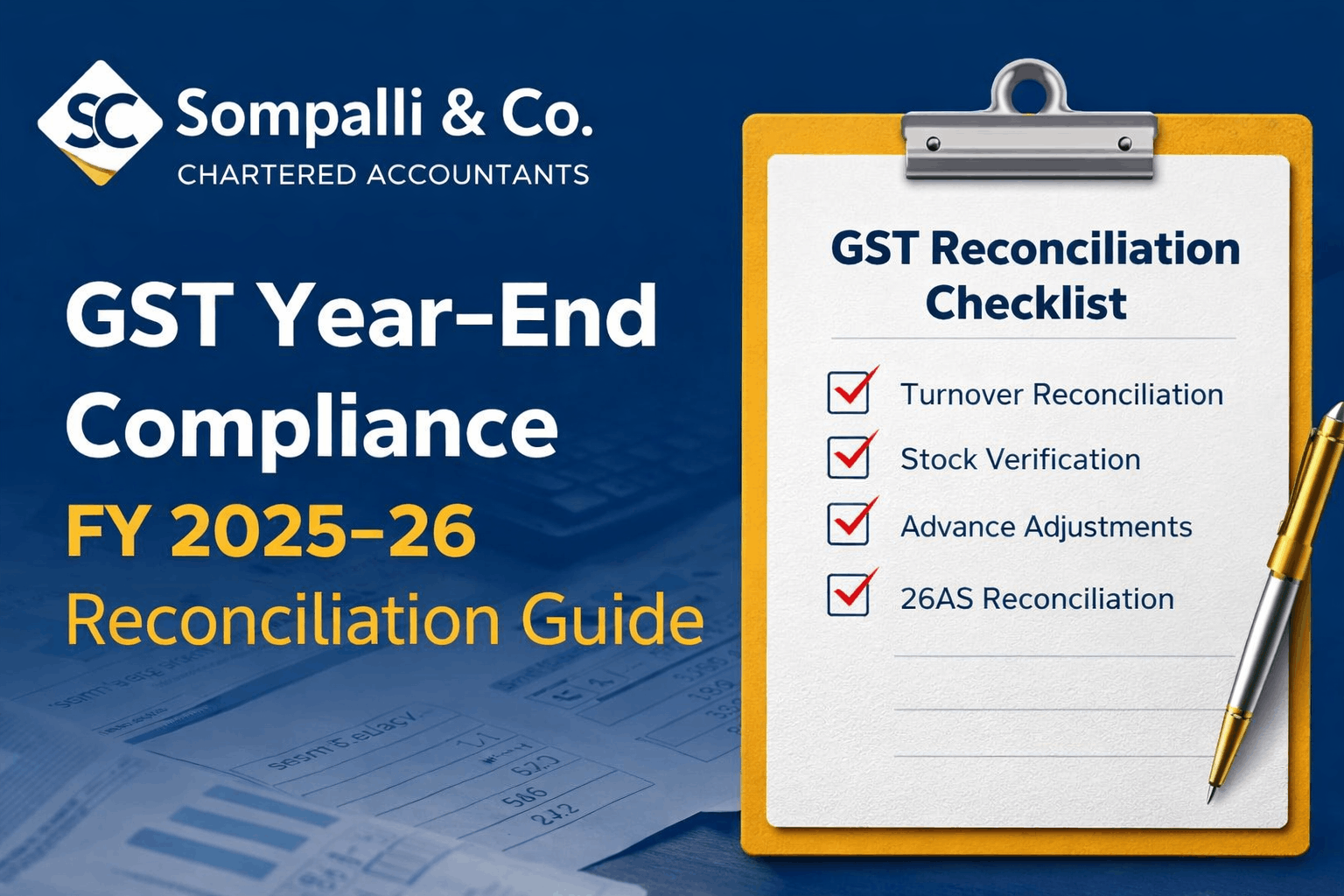

GST Year-End Compliance FY 2025–26: Key Reconciliations Every Business Must Review

Ensure accurate GST reporting with key year-end reconciliations for FY 2025–26 to avoid notices, mismatches, and penalties.

Loading Sompalli & Co...

Expert insights, industry updates, and professional advice from Sompalli & Co.

Ensure accurate GST reporting with key year-end reconciliations for FY 2025–26 to avoid notices, mismatches, and penalties.

summary of key developments under GST for May 2025, including compliance changes, judicial rulings, and upcoming transitions

All Types of GST Refunds in India – A Complete Guide with Sections & Rules

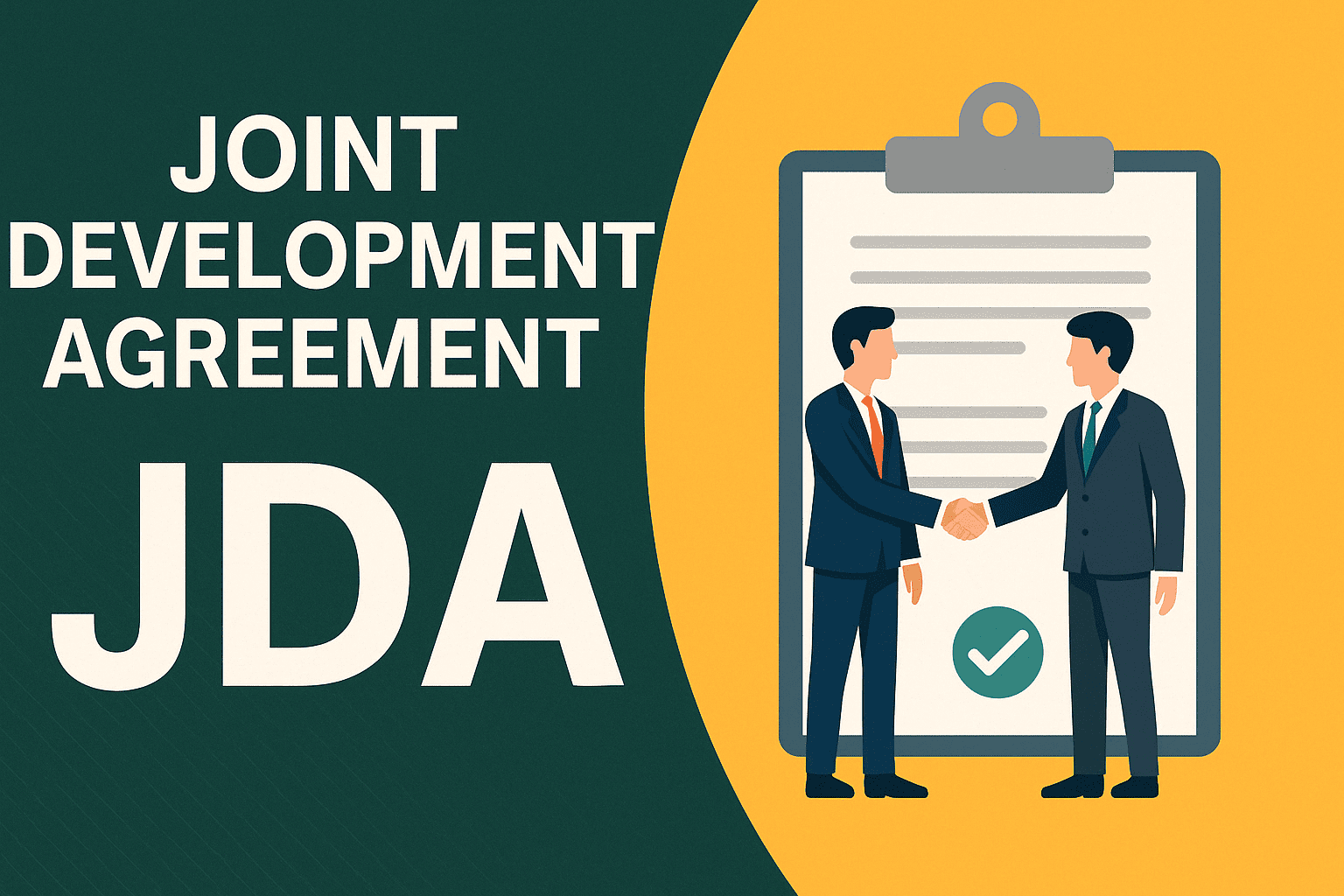

A Joint Development Agreement (JDA) is a legal arrangement between a landowner and a real estate developer (builder) wherein the landowner contributes land, and the developer undertakes construction and development. Instead of monetary compensation, the landowner typically receives a share in the constructed property (residential/commercial units or revenue share).

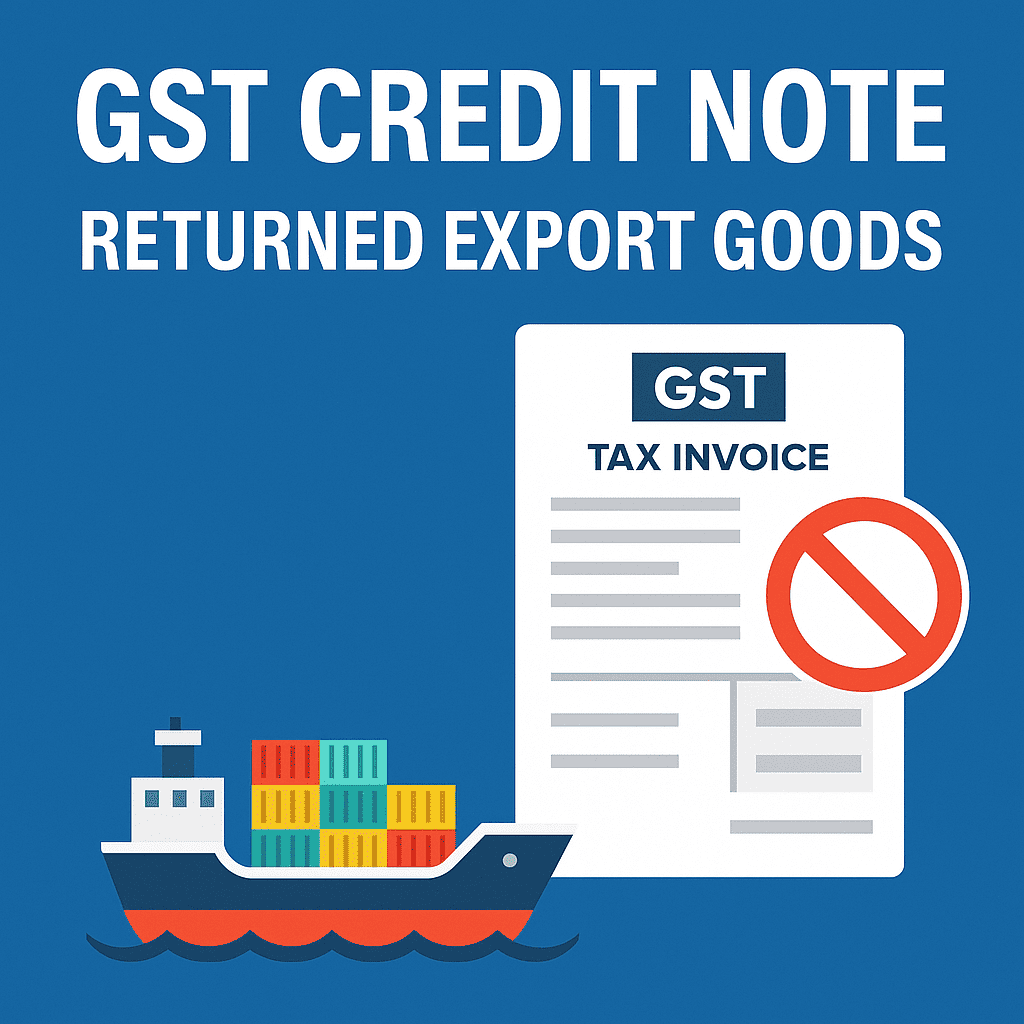

In the complex landscape of GST compliance, one common dilemma arises when exported goods are returned by the foreign buyer after IGST has already been paid and refund has been claimed. A key question is: Can a GST credit note be issued under Section 34 of the CGST Act in such a case? The answer is No — and this article comprehensively explains why, along with legal references, practical treatment, and alternate solutions for businesses and consultants.

In the Goods and Services Tax (GST) regime, the Reverse Charge Mechanism (RCM) shifts the tax liability from the supplier to the recipient of goods or services. Unlike the regular forward charge, where the supplier is liable to pay GST, under RCM, the recipient is required to pay the applicable GST directly to the government. RCM is governed by Section 9(3), 9(4), and 9(5) of the Central Goods and Services Tax Act, 2017 (CGST Act) for intra-state supplies and Section 5(3), 5(4), and 5(5) of the Integrated Goods and Services Tax Act, 2017 (IGST Act) for inter-state supplies.

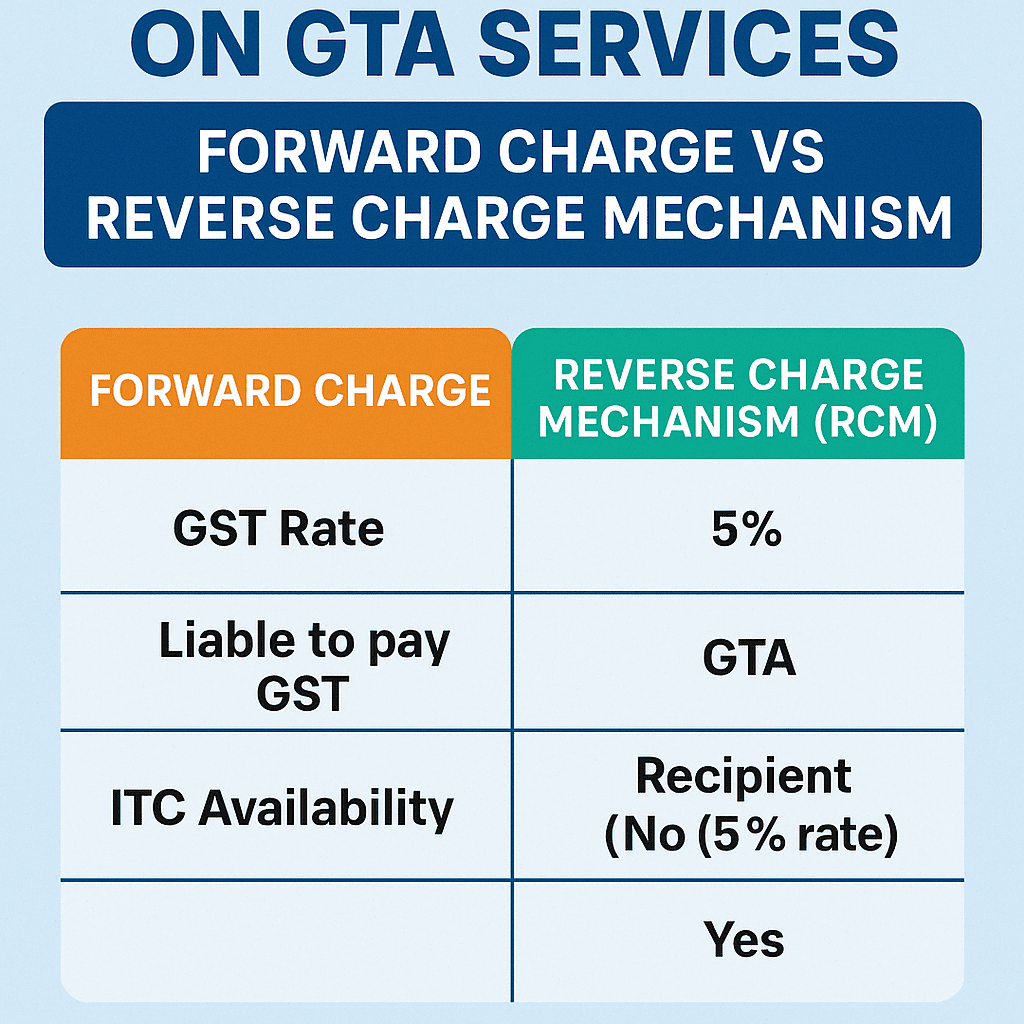

🔹 Introduction Under the GST regime, the transport of goods by road is a critical business service. When this service is provided by a Goods Transport Agency (GTA), it attracts special treatment under GST law. The liability to pay GST can arise under either the Forward Charge Mechanism (FCM) or the Reverse Charge Mechanism (RCM) based on specific conditions.