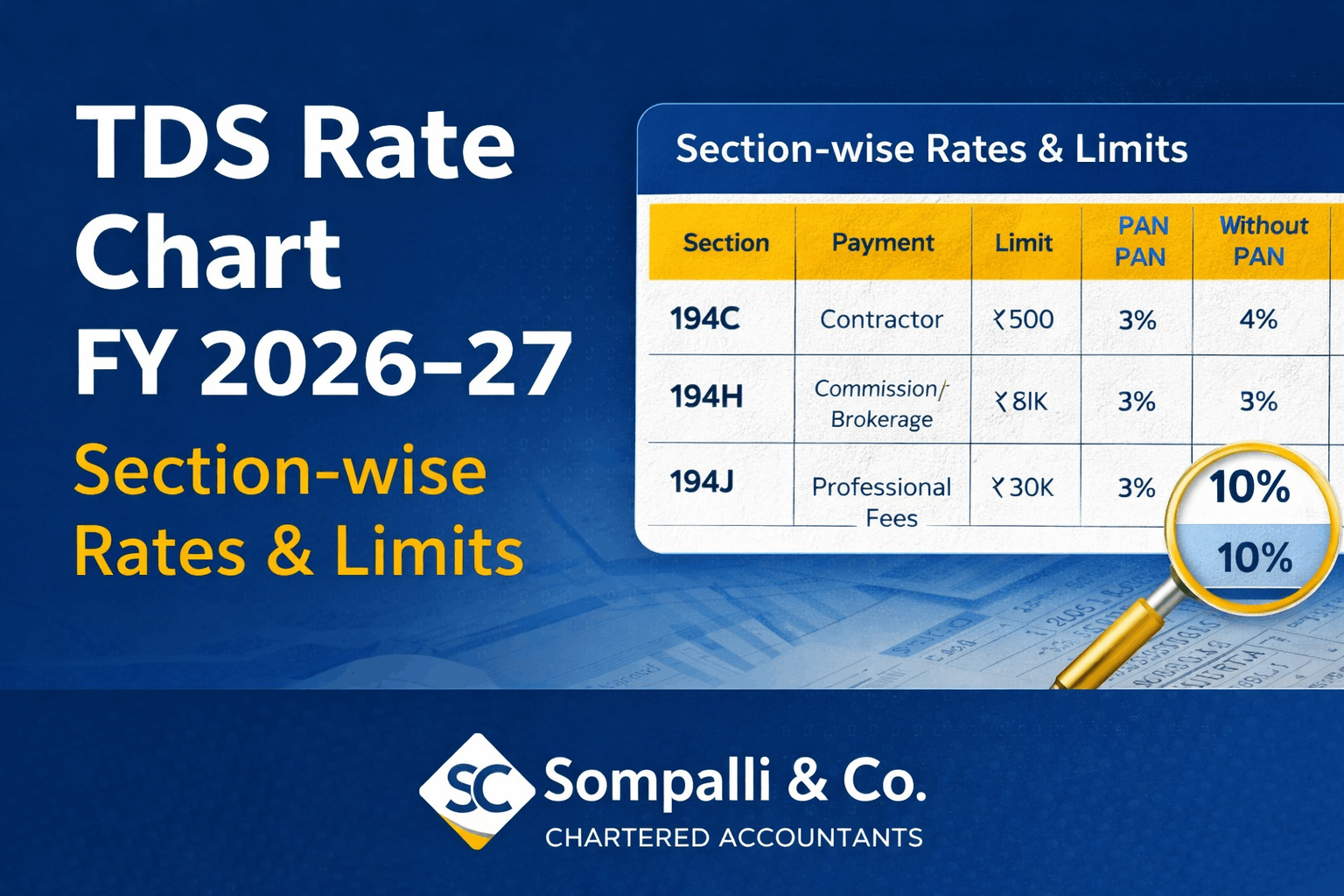

Most Used TDS Sections — Tax Year 2026-27

The Income Tax Act, 2025 has restructured the entire TDS framework. Familiar sections like 194C, 194H, 194J, and 194I have been re-numbered under the new consolidated sections 392, 393, and 394. Below is a quick-reference chart of the most commonly used TDS provisions, mapped from old to new with the latest rates and thresholds.