GST on Goods Transport Agency (GTA) Services — Updated Guide (Post GST 2.0, effective 22 Sept 2025)

1. Definition of GTA

As per Notification No. 11/2017–Central Tax (Rate) dated 28.06.2017, as amended by Notification No. 16/2025–Central Tax (Rate) dated 16.07.2025:

"GTA means any person who provides service in relation to transport of goods by road and issues a consignment note, by whatever name called, but does not include (i) an electronic commerce operator by whom the services of local delivery are provided, or (ii) an electronic commerce operator through whom the services of local delivery are provided."

Two things matter here in practice:

- No consignment note, no GTA status. A truck owner or fleet operator who moves goods but never issues a consignment note is just a "goods transport operator" — outside GTA provisions entirely, and the freight is exempt from GST.

- E-commerce local delivery is now carved out. Since July 2025, hyperlocal delivery arranged through an e-commerce operator (think quick-commerce delivery partners) is explicitly excluded from GTA classification, so it's taxed under separate e-commerce provisions, not the GTA framework below.

A valid consignment note must show: consignor and consignee names, description of goods, place of origin and destination, vehicle registration number, a serial number, and who is liable to pay GST (consignor, consignee, or the GTA itself).

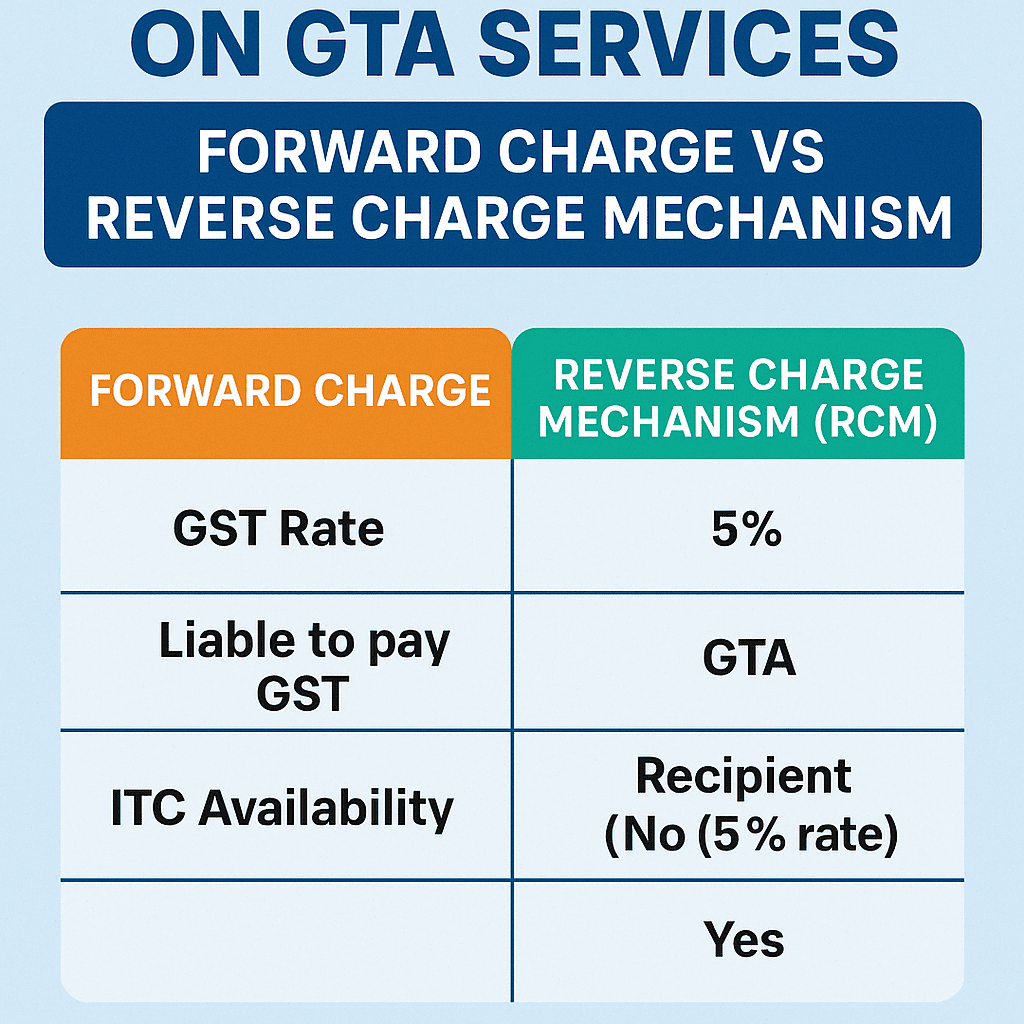

2. GST Rates on GTA Services (Rates Changed 22 September 2025)

This is the single biggest update. Under GST 2.0, the old four-slab structure (5/12/18/28%) was compressed into two main slabs (5%/18%). For GTA specifically, the 12% forward-charge option has been replaced by 18%. The 5% no-ITC route is unchanged.

| Mechanism | GST Rate | Who Pays | ITC to GTA? | ITC to Recipient? |

|---|---|---|---|---|

| RCM (default, GTA hasn't opted for FCM) | 5% | Recipient (notified categories) | No | Yes, if used for business |

| FCM – Option 1 | 5% | GTA | No | No (5% route carries no ITC anywhere in the chain) |

| FCM – Option 2 | 18% (was 12% before 22 Sept 2025) | GTA | Yes | Yes, subject to normal ITC rules |

Practical takeaway: if your GTA has been invoicing at 12% for years, that invoice format needs updating from September 2025 onward — anything charged at 12% now is simply incorrect. If your accounting software or a vendor's rate card still shows 12%, flag it for correction immediately; it's a common leftover error post-transition.

GST-exempt GTA services (0%) — unchanged by GST 2.0

- Agricultural produce, milk, salt, food grain (flour, pulses, rice), organic manure

- Newspapers/magazines registered with the Registrar of Newspapers

- Relief material for natural/man-made disaster victims; defence or military equipment

- Used household goods moved for personal use

- Hiring a vehicle out to a GTA (input side of the GTA's own business)

- Single-carriage consignment where freight for one consignment is under ₹1,500

- Single-consignee freight under ₹750 even if part of a larger truckload

Practical example: A small trader pays a local transporter ₹600 to bring one lot of goods from a wholesaler. Because it's under the ₹750 single-consignee threshold, no GST applies — even if the trader is GST-registered and would otherwise fall under RCM.

3. Reverse Charge Mechanism (RCM) — Default Scenario

Applies automatically whenever the GTA has not filed a forward-charge declaration (Annexure V — see Section 5).

Recipients liable to pay under RCM (Notification No. 13/2017–CT (Rate))

| # | Category |

|---|---|

| 1 | Factory registered under the Factories Act, 1948 |

| 2 | Society registered under the Societies Registration Act (or similar law) |

| 3 | Co-operative society |

| 4 | Any GST-registered person |

| 5 | Body corporate established by or under any law |

| 6 | Partnership firm, registered or not (including LLP/AOP) |

| 7 | Casual taxable person |

Who actually pays, in practice — it's whoever is contractually liable to pay the freight, not necessarily consignor or consignee automatically:

- If the consignor pays the freight and falls in the above list, the consignor pays RCM.

- If the consignee pays the freight and falls in the above list, the consignee pays RCM.

- If neither party pays (freight paid by an unregistered person outside the list), and no listed entity is footing the bill, the transaction may fall outside RCM — check the specific facts.

Exception: when the recipient is Central Government, a State Government, a Union Territory, or a local authority, RCM does not apply — liability sits with the GTA under forward charge instead.

ITC under RCM

- GST paid under RCM is available as ITC to the recipient, if the freight relates to a taxable business activity.

- RCM tax must be paid in cash (not through ITC ledger); the credit can then be claimed once the self-invoice/payment is recorded, subject to normal ITC timing rules.

4. Forward Charge Mechanism (FCM) — Optional, GTA's Choice

A GTA may elect to charge and pay GST itself instead of pushing liability to the recipient.

How to opt in — Annexure V

- File Annexure V with the jurisdictional GST office declaring the choice to pay under forward charge for the entire financial year.

- Deadline: 15 March of the year preceding the financial year it applies to (e.g., for FY 2027–28, file by 15 March 2027).

- New GTAs (newly registered mid-year) get 45 days from applying for GST registration, or one month from actually receiving registration — whichever is later — to file Annexure V for the current year.

- Once opted, FCM applies to all GTA supplies for the entire year and cannot be reversed mid-year back to RCM.

- If Annexure V isn't filed by the deadline, the GTA automatically defaults to RCM for that year.

Choosing the rate under FCM

- 5%, no ITC — simpler, lower headline rate, but the GTA can't recover GST paid on trucks, fuel-related services, repairs, etc.

- 18%, full ITC (replaces the old 12% rate from 22 Sept 2025) — higher invoice value but the GTA can claim credit on inputs, and the recipient gets full ITC too.

A GTA can actually use both rates within the same year for different consignments/customers, as long as the invoice-level declaration is consistent and it has opted into FCM overall — it's not locked to a single rate for every invoice.

Annexure III declaration

Once a GTA has opted for FCM, every tax invoice must carry the Annexure III declaration confirming forward charge is being applied. This is what tells the recipient not to self-invoice under RCM — without it, a recipient may mistakenly apply RCM anyway, causing a duplicate tax dispute.

5. GTA-to-GTA Sub-Contracting — When Is It Exempt?

A common scenario: Customer ABC hires GTA XYZ, and XYZ sub-contracts the actual truck movement to another operator, PQR. Is PQR's service to XYZ exempt? Not automatically — it turns entirely on whether PQR issues its own consignment note.

- PQR does not issue a consignment note (it's just supplying a vehicle/driver to move goods under XYZ's original consignment note to ABC): PQR isn't legally a "GTA" for this leg at all. The service falls under the general exemption for road transport by a non-GTA operator (Notification No. 12/2017–CT (Rate), Entry 18 — transport of goods by road is exempt except when done by a GTA or courier agency). PQR's supply to XYZ is exempt.

- PQR does issue its own consignment note to XYZ (acting as an independent GTA rather than a hired vehicle): PQR is a GTA in its own right for that transaction, and ordinary GTA taxability applies — RCM (XYZ, typically a body corporate/firm, would usually be the RCM-liable recipient) or FCM if PQR has opted in via Annexure V.

This has been tested in practice: a Maharashtra AAR ruling held that there cannot be two consignment notes for the same movement, and confirmed that a sub-contractor providing vehicles under the main contractor's note is not itself a GTA, so its service is exempt. Separately, rulings have also confirmed that mere non-issuance of a consignment note doesn't automatically create an exemption if the sub-contractor is, in substance, independently contracting and invoicing as a transporter — the facts of who controls the consignment note matter more than paperwork labels.

Practical bottom line: the rule isn't "GTA-to-GTA is always exempt." It's "whoever doesn't issue the consignment note isn't taxed as a GTA." Most genuine sub-contracting (a truck owner working under the primary GTA's note) qualifies as exempt; a second GTA independently invoicing with its own note does not.

Practical example: GTA XYZ takes a booking from ABC Ltd. and issues a consignment note covering the full Delhi-to-Mumbai movement. XYZ doesn't own enough trucks, so it books a truck from PQR Transport for the Delhi-to-Nagpur leg. PQR doesn't issue any consignment note of its own — it just moves the goods under XYZ's paperwork and invoices XYZ for the hire. PQR's invoice to XYZ is GST-exempt. If instead PQR issued its own consignment note to XYZ for that leg, PQR would be a GTA supplying to XYZ, and XYZ (likely a body corporate or firm) would owe GST under RCM on that leg, unless PQR had opted for FCM.

5.1 ITC Reversal — Taxable Sub-Contract vs. Exempt Sub-Contract

Whether XYZ needs to reverse (or simply forgo) input tax credit depends on two separate questions: (a) was GST actually charged on the sub-contracted leg, and (b) what rate did XYZ itself choose for its outward supply to ABC. Reversal risk only exists where GST was paid and XYZ's own output is on a no-ITC rate.

Common facts: Nagpur leg (sub-contracted) valued at ₹1,00,000. Full Delhi–Mumbai freight billed to ABC valued at ₹3,00,000.

| Illustration A — Taxable sub-contract (PQR issues its own consignment note) | Illustration B — Exempt sub-contract (PQR issues no consignment note) | |

|---|---|---|

| PQR's invoice to XYZ | ₹1,00,000 + 18% GST = ₹1,18,000 (PQR opted FCM @18% with ITC) | ₹1,00,000 flat, no GST — exempt under Entry 18 |

| Input GST available to XYZ on this leg | ₹18,000 (a real credit sitting in XYZ's electronic credit ledger) | ₹0 — nothing was ever charged, so there is nothing to credit or reverse |

| XYZ bills ABC at 18% (FCM, with ITC) | XYZ charges ₹54,000 GST, claims the ₹18,000 as ITC. Net GST paid to government: ₹36,000. No reversal — full credit chain intact. | XYZ charges ₹54,000 GST. No PQR-related credit exists to claim, but XYZ can still claim ITC on genuine taxable inputs (fuel-linked services, repairs, insurance) used for this trip. No reversal issue. |

| XYZ bills ABC at 5% (FCM, no-ITC) | XYZ charges ₹15,000 GST but, as a condition of the 5% no-ITC rate, cannot retain the ₹18,000 credit already sitting from PQR's invoice. If already claimed, it must be reversed; the ₹18,000 becomes a straight cost instead of a credit. | XYZ charges ₹15,000 GST. Since PQR's supply was never taxed, there was never a credit to reverse on this leg — the no-ITC condition is simply moot here. Only other taxable inputs used for the trip are affected. |

The takeaway: reversal is only ever a live issue in Illustration A — where tax was actually paid up the chain and then XYZ elects (or is required to use) a no-ITC output rate. In Illustration B, since PQR's supply carried no GST to begin with, there is structurally nothing to reverse; the sub-contracting arrangement is simply tax-neutral at that leg.

One more layer — proportionate reversal under Rule 42/43. If XYZ, over a tax period, makes a mix of taxable (18%) and exempt/no-ITC (5% or wholly exempt, e.g. agricultural produce) outward supplies, and incurs common input services that can't be tied to one supply or the other (office rent, admin software, generic fleet insurance), it must reverse a proportionate share of ITC on those common inputs under Rule 42 (CGST Rules), based on the ratio of exempt/no-ITC turnover to total turnover for that period — separate from, and in addition to, the leg-specific analysis above.

6. Time of Supply and Self-Invoicing under RCM (Rule 47A)

For recipients paying under RCM, the time of supply is the earliest of:

- Date the service is entered in the recipient's books

- Date payment is made or debited from the bank

- 30 days from the date of the GTA's invoice/document

- Date the recipient issues a self-invoice, if applicable

Self-invoicing is mandatory — the recipient must issue a self-invoice within 30 days of receiving the service, regardless of whether the GTA issues its own bill. This trips up a lot of businesses: even if the GTA never sends a formal invoice, the RCM liability and self-invoicing obligation still exist by law.

7. HSN Code Reporting (Effective January 2025)

| GTA Turnover | HSN/SAC Digits Required |

|---|---|

| Up to ₹5 crore | 4-digit |

| Above ₹5 crore | 6-digit |

8-digit codes are not required for domestic GTA services. Incorrect HSN reporting in GSTR-1 can attract penalties up to ₹10,000 or the GST evaded, whichever is higher.

8. Compliance Checklist

If under RCM (recipient's obligations)

| Requirement | Detail |

|---|---|

| Self-invoice | Issue within 30 days of receiving the service |

| GSTR-3B | Report RCM liability in Table 3.1(d) |

| Payment voucher | Issue at the time of payment to the GTA |

| Cash payment | RCM liability must be discharged in cash, not via ITC ledger |

| Records | Maintain RCM liability ledger, self-invoices, payment vouchers |

If under FCM (GTA's obligations)

| Requirement | Detail |

|---|---|

| Annexure V | File by 15 March of the preceding FY (or within 45 days of registration for new GTAs) |

| Rate choice | 5% (no ITC) or 18% (full ITC), per invoice |

| Annexure III | Include the FCM declaration on every invoice |

| GSTR-1 | Report outward supply in Table 4 |

| GSTR-3B | Report tax in Table 3.1(a) |

| HSN | 4-digit or 6-digit per turnover threshold |

9. Practical Examples

Example 1 — Standard RCM case.

XYZ Ltd. (a registered company) hires ABC Transport, a GTA that has not filed Annexure V. ABC issues a proper consignment note. Since XYZ is a body corporate and pays the freight, XYZ pays 5% GST under RCM via self-invoice, and can claim that 5% as ITC if the freight relates to business activity.

Example 2 — GTA opted for FCM at 18%.

PQR Logistics has filed Annexure V and charges 18% GST on its invoices (with the Annexure III declaration). A recipient business can claim full ITC on that 18%, and PQR itself can claim ITC on truck purchases, repairs, and other taxable inputs used in the business.

Example 3 — Low-value consignment, no GST.

A retailer pays a local transporter ₹1,200 to move a single consignment of stock. Since this is below the ₹1,500 single-carriage threshold, the freight is GST-exempt — no RCM, no invoice tax, regardless of the retailer's GST registration status.

Example 4 — Unregistered small trader.

A sole proprietor with turnover below the registration threshold hires a GTA to bring goods from a supplier. Because the trader isn't in any of the seven notified RCM categories and isn't GST-registered, no RCM liability arises on this transaction — but note the GTA itself must still separately assess its own registration obligations if it has any RCM-exempt or taxable supplies.

Example 5 — Stale 12% invoice (post-Sept-2025 error).

A company receives an FCM invoice from its transporter dated November 2025 showing 12% GST. This is now incorrect — the transporter's software wasn't updated after the GST 2.0 rate change. The correct forward-charge rate with ITC from 22 September 2025 onward is 18%, not 12%. The recipient should flag this before claiming ITC, since claiming credit on an incorrectly-rated invoice can be challenged on audit.

10. Summary Table

| Scenario | GST Rate | Who Pays | GTA gets ITC? | Recipient gets ITC? |

|---|---|---|---|---|

| RCM (default) | 5% | Recipient (7 notified categories) | No | Yes |

| FCM, no-ITC option | 5% | GTA | No | No |

| FCM, ITC option (was 12%, now 18% since 22 Sept 2025) | 18% | GTA | Yes | Yes |

| Exempt goods / low-value consignments | 0% | — | — | — |

11. Key Takeaways

- The old 12% forward-charge slab is gone — it's 18% with ITC from 22 September 2025 onward. Check vendor invoices and software configurations for stale 12% entries.

- The GTA definition now explicitly excludes e-commerce hyperlocal delivery (July 2025 amendment).

- Annexure V (opt into FCM) and Annexure III (invoice declaration) are both still required — this hasn't changed.

- GTA-to-GTA sub-contracting is exempt only if the sub-contractor doesn't issue its own consignment note — not a blanket exemption.

- Self-invoicing under RCM within 30 days is a frequently missed compliance step; the obligation exists even if the GTA never issues its own invoice.

- HSN reporting thresholds (4-digit vs 6-digit, based on ₹5 crore turnover) took effect January 2025 and apply regardless of RCM/FCM status.

This guide reflects notifications and rate changes through the GST 2.0 rationalization effective 22 September 2025. GST rules are amended frequently — verify current notification numbers on the CBIC portal before relying on this for a filing position, and consult a tax professional for transaction-specific advice.

Sources:

- Comprehensive Guide to GST on Freight: Key Updates as of August 2025 – TaxGuru

- Goods Transport Agency under GST – ClearTax

- Supply of Service by Goods Transport Agency (GTA) – Detailed Analysis – TaxGuru

- A sub-contractor providing vehicles for transporting goods to GTA is not a GTA himself – Sabka GST

Urukundu

Urukundu