Effective from 1st April 2025

Key Changes in TDS for FY 2025-26

Enhanced Threshold Limits (Effective from 1st April 2025)

| Section | Nature of Payment | Previous Limit (₹) | New Limit (₹) |

|---|---|---|---|

| 193 | Interest on securities | NIL | 10,000 |

| 194A | Interest (Bank/Coop/Post Office) - Senior Citizens | 50,000 | 1,00,000 |

| 194A | Interest (Bank/Coop/Post Office) - Others | 40,000 | 50,000 |

| 194A | Interest (Others) | 5,000 | 10,000 |

| 194 | Dividend | 5,000 | 10,000 |

| 194K | Mutual Fund Income | 5,000 | 10,000 |

| 194B | Lottery/Crossword Winnings | 10,000 (aggregate) | 10,000 (per transaction) |

| 194BB | Horse Race Winnings | 10,000 (aggregate) | 10,000 (per transaction) |

| 194D | Insurance Commission | 15,000 | 20,000 |

| 194G | Commission on Lottery Tickets | 15,000 | 20,000 |

| 194H | Commission/Brokerage | 15,000 | 20,000 |

| 194I | Rent | 2,40,000 (yearly) | 50,000 (monthly) |

| 194J | Professional/Technical Services | 30,000 | 50,000 |

| 194LA | Enhanced Compensation | 2,50,000 | 5,00,000 |

TDS Rates for Payments to Non-Residents

| Section | Nature of Payment | TDS Rate |

|---|---|---|

| 192 | Salary | As per income tax slabs + Surcharge + Cess |

| 194A | Interest | 20% + Surcharge + Cess |

| 194B | Lottery winnings | 30% + Surcharge + Cess |

| 194BB | Horse race winnings | 30% + Surcharge + Cess |

| 194C | Contract payments | 30% + Surcharge + Cess |

| 194E | Sportsman/Sports association | 20% + Surcharge + Cess |

| 194F | Mutual fund repurchase | 20% + Surcharge + Cess |

| 194H | Commission/Brokerage | 30% + Surcharge + Cess |

| 194I | Rent | 30% + Surcharge + Cess |

| 194J | Professional/Technical services | 30% + Surcharge + Cess |

| 194LB | Securitization trust | 30% + Surcharge + Cess |

| 194LBA | Business trust | 30% + Surcharge + Cess |

| 194LBB | Investment fund | 30% + Surcharge + Cess |

| 194LBC | Securitization trust | 30% + Surcharge + Cess |

| 195 | Other payments | 30% + Surcharge + Cess |

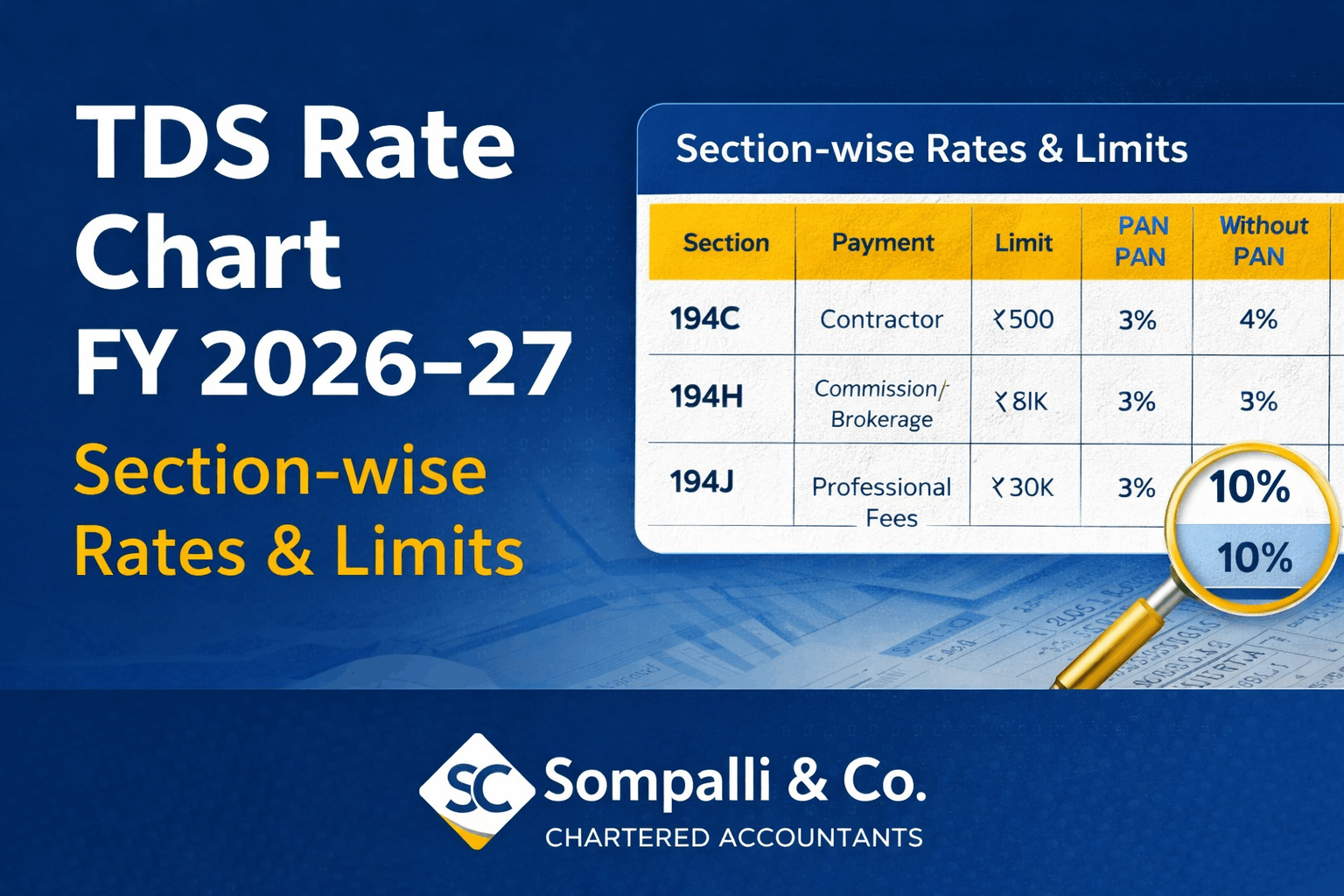

TDS Rates for Payments to Residents (FY 2025–26 | AY 2026–27)

| Section | Nature of Transaction | Threshold Limit (₹) | TDS Rate |

|---|---|---|---|

| 192 | Salary | As per income tax slabs | 10% to 30% |

| 192A | Premature withdrawal from EPF | 50,000 | 10% |

| 193 | Interest on securities | 10,000 | 10% |

| 194 | Dividend | 10,000 | 10% |

| 194A | Interest other than securities | 10,000 / 50,000 / 1,00,000 | 10% |

| 194B | Lottery / Crossword winnings | 10,000 | 30% |

| 194BB | Horse race winnings | 10,000 | 30% |

| 194C | Contract payments | 30,000 (Ind./HUF) / 1,00,000 (Others) | 1% (Ind./HUF) / 2% (Others) |

| 194D | Insurance commission | 20,000 | 5% |

| 194DA | Life insurance policy payments | 1,00,000 | 5% |

| 194E | Non-resident sportsman / sports association | No threshold | 20% |

| 194EE | NSS / NSC / SCSS interest | 2,500 | 10% |

| 194F | Mutual fund units repurchase | No threshold | 20% |

| 194G | Lottery ticket commission | 20,000 | 5% |

| 194H | Commission / Brokerage | 20,000 | 5% |

| 194I | Rent (Land/Building/Furniture) | 50,000 (monthly) | 10% |

| 194IA | Sale of immovable property | 50,00,000 | 1% |

| 194IB | Rent by individual / HUF | 50,000 (monthly) | 5% |

| 194IC | Joint development agreement | 50,00,000 | 10% |

| 194IS | Rent by Ind./HUF (other than 194IB) | 50,000 (monthly) | 2% |

| 194J | Professional / Technical services | 50,000 | 10% (Prof.) / 2% (Tech.) |

| 194K | Mutual fund income | 10,000 | 10% |

| 194LA | Compensation (land acquisition) | 5,00,000 | 10% |

| 194LB | Income from securitization trust | 2,500 | 25% (Ind./HUF) / 30% (Others) |

| 194LBA | Business trust income | 2,500 | 10% |

| 194LBB | Investment fund income | 2,500 | 10% |

| 194LBC | Securitization trust income | 2,500 | 10% |

| 194M | Contract / Professional services | 50,00,000 | 5% |

| 194N | Cash withdrawal | 1,00,00,000 | 2% |

| 194O | E-commerce transactions | 5,00,000 | 1% |

| 194P | Winnings from horse race | 10,000 | 30% |

| 194Q | Purchase of goods | 50,00,000 | 0.1% |

| 194R | Benefits / Perquisites | 20,000 | 10% |

| 194S | Crypto / Virtual digital assets | 10,000 | 1% |

| 194T | Partner remuneration | 20,000 | 10% |

TDS Rates for Companies (Domestic & Foreign)

| Section | Nature of Payment | Domestic Company | Foreign Company |

|---|---|---|---|

| 194C | Contract payments | 2% | 30% + Surcharge + Cess |

| 194J | Professional services | 10% | 30% + Surcharge + Cess |

| 194J | Technical services | 2% | 30% + Surcharge + Cess |

| 194I | Rent | 10% | 30% + Surcharge + Cess |

Special Provisions

- Higher TDS Rate for Non-furnishing of PAN: 20% if PAN is not furnished by the payee (unless specified otherwise)

- New Section 194T – Partner's Remuneration (Effective from 1st April 2025):

- Threshold: ₹20,000 per financial year

- Rate: 10%

- Applicable on: Salary, remuneration, bonus, commission, interest paid to partners

- Not applicable on: Drawings and capital repayment to partners

- Sections Removed from 1st April 2025:

- Section 206AB: Higher TDS for non-filers

- Section 206CCA: Higher TCS for non-filers

- Section 206C(1H): TCS on sale of goods

- TCS Changes:

- LRS Remittance threshold raised from ₹7 lakhs to ₹10 lakhs

- No TCS on remittance of educational loans from financial institutions

- Luxury Goods: TCS of 1% on purchases exceeding ₹10 lakhs (effective January 2025)

Important Notes

- Cess: Health & Education Cess @ 4% is applicable on Income Tax + Surcharge

- Due Dates:

- TDS Payment: 7th of the following month

- Quarterly TDS Returns: As per prescribed dates

- TAN: Tax Deduction Account Number is mandatory for deducting TDS

- Form 15G/15H: Can be submitted to avoid TDS if income is below taxable limit

- Interest on Late Payment: 1.5% per month for delay in depositing TDS

- Interest on Late Deduction: 1% per month for delayed deduction

Income Tax Slabs for FY 2025–26 (New Tax Regime)

| Income Range | Tax Rate |

|---|---|

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 to ₹8,00,000 | 5% |

| ₹8,00,001 to ₹12,00,000 | 10% |

| ₹12,00,001 to ₹16,00,000 | 15% |

| ₹16,00,001 to ₹20,00,000 | 20% |

| ₹20,00,001 to ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

Rebate under Section 87A: ₹60,000 (New Regime) / ₹12,500 (Old Regime)

This chart is based on the Finance Act 2025 and amendments effective from 1st April 2025. Please consult a qualified tax professional or refer to the latest Income Tax notifications for updates or clarifications.

praveen Sompalli

praveen Sompalli