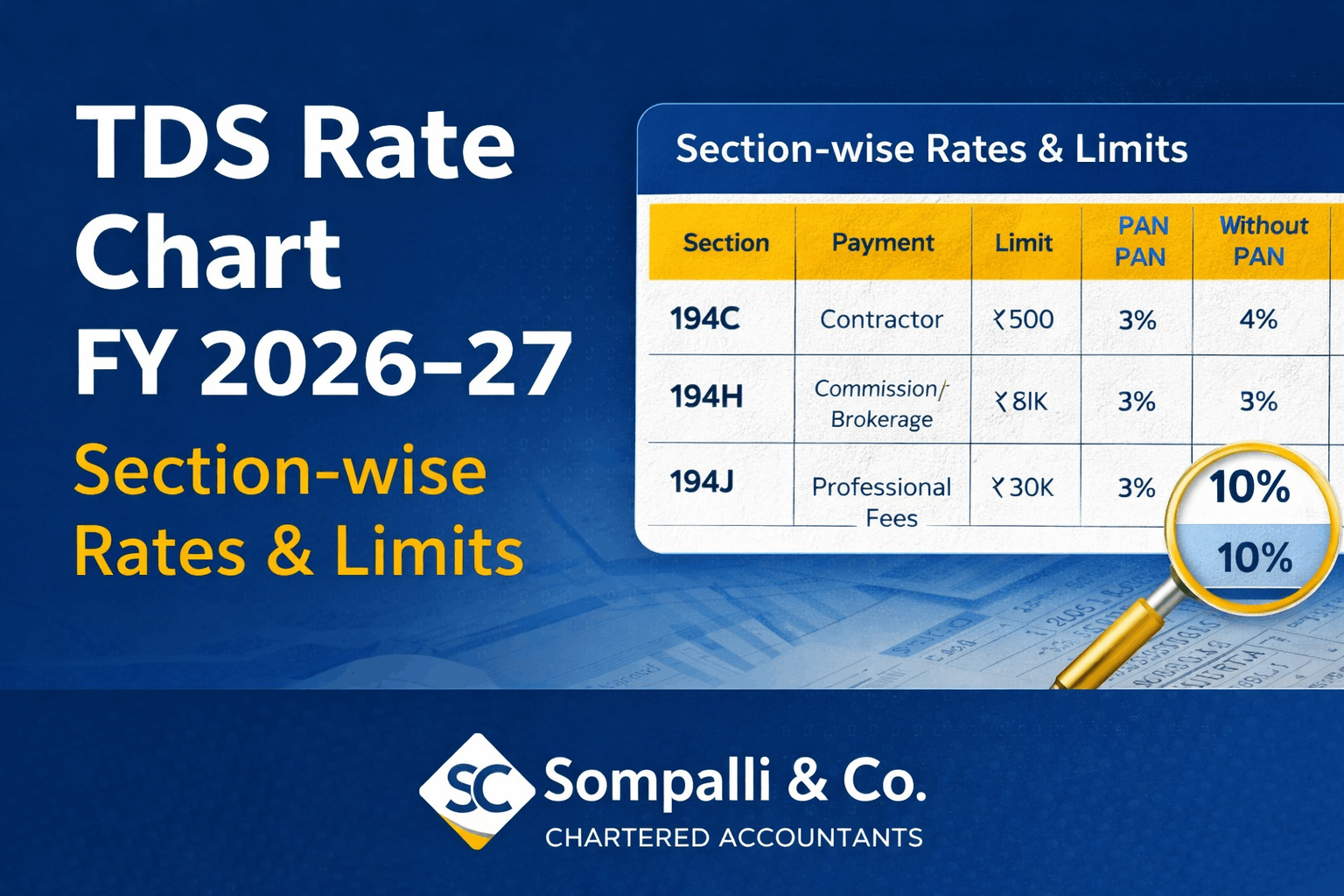

The Income Tax Act, 2025 has restructured the entire TDS framework. Familiar sections like 194C, 194H, 194J, and 194I have been re-numbered under the new consolidated sections 392, 393, and 394. Below is a quick-reference chart of the most commonly used TDS provisions, mapped from old to new with the latest rates and thresholds.

Most Used TDS Sections — Tax Year 2026-27

The Income Tax Act, 2025 has restructured the entire TDS framework. Familiar sections like 194C, 194H, 194J, and 194I have been re-numbered under the new consolidated sections 392, 393, and 394. Below is a quick-reference chart of the most commonly used TDS provisions, mapped from old to new with the latest rates and thresholds.

Key Rate Changes (IT Act 2025 vs IT Act 1961)

| Section |

Nature |

Old Rate |

New Rate |

| 194H | Commission | 5% | 2% |

| 194IB | Rent (Individual / HUF) | 5% | 2% |

| 194J(a) | Technical Services | 10% | 2% |

| 194M | Payment by Individual / HUF | 5% | 2% |

| 194G | Lottery commission | 5% | 2% |

| 194DA | Insurance maturity | 5% | 2% |

Salary / EPF

| Code |

Old Sec. |

Nature of Payment |

New Section (IT Act 2025) |

Rate |

Threshold (Rs.) |

| 1001 | 192 | Salary — State Govt. / other Govt. employees | 392 | Slab | — |

| 1002 | 192 | Salary — Private / Non-Govt. employees | 392 | Slab | — |

| 1003 | 192 | Salary — Union (Central) Govt. employees | 392 | Slab | — |

| 1004 | 192A | EPF withdrawal — premature (before 5 years of service) | 392(7) | 10% | — |

Commission & Rent

| Code |

Old Sec. |

Nature of Payment |

New Section (IT Act 2025) |

Rate |

Threshold (Rs.) |

| 1005 | 194D | Commission / Brokerage — Insurance companies | 393(1)[Sl.1(i)] | 2% (Indv.)

10% (Others) | 20,000 |

| 1006 | 194H | Commission or Brokerage — others (non-insurance) | 393(1)[Sl.1(ii)] | 2% | 20,000 |

| 1007* | 194IB | Rent — Individual/HUF (non-audit), above Rs.50,000/month | 393(1)[Sl.2(i)] | 2% | 50,000/month |

| 1008 | 194I(a) | Rent of Plant, Machinery or Equipment | 393(1)[Sl.2(ii).D(a)] | 2% | 50,000/month |

| 1009 | 194I(b) | Rent of Land / Building / Furniture | 393(1)[Sl.2(ii).D(b)] | 10% | 50,000/month |

Interest & Mutual Fund

| Code |

Old Sec. |

Nature of Payment |

New Section (IT Act 2025) |

Rate |

Threshold (Rs.) |

| 1019 | 193 | Interest on Securities (Bonds, Debentures etc.) | 393(1)[Sl.5(i)] | 10% | 10,000 |

| 1020 | 194A | Bank/PO deposit interest — Senior Citizen deductee | 393(1)[Sl.5(ii).D(a)] | 10% | 1,00,000 |

| 1021 | 194A | Bank/PO deposit interest — Other than Senior Citizen | 393(1)[Sl.5(ii).D(b)] | 10% | 50,000 |

| 1022 | 194A | Interest by other payers (non-bank / non-PO) | 393(1)[Sl.5(iii)] | 10% | 10,000 |

| 1029 | 194 | Dividend by domestic company (incl. preference shares) | 393(1)[Sl.7] | 10% | 10,000 (Indv.) |

| 1013 | 194K | Income from units of Mutual Fund / specified undertaking | 393(1)[Sl.4(i)] | 10% | 10,000 |

| 1014 | 194LBA | Business Trust (REIT/InvIT) — interest income, resident | 393(1)[Sl.4(ii)] | 10% | — |

| 1017 | 194LBB | AIF income to resident unit holders (non-exempt portion) | 393(1)[Sl.4(iii)] | 10% | — |

Contracts & Professional

| Code |

Old Sec. |

Nature of Payment |

New Section (IT Act 2025) |

Rate |

Threshold (Rs.) |

| 1023 | 194C | Contract payment — Individual / HUF contractor | 393(1)[Sl.6(i).D(a)] | 1% | 30,000 (single)

1,00,000 (agg.) |

| 1024 | 194C | Contract payment — Company / Firm / Other contractor | 393(1)[Sl.6(i).D(b)] | 2% | 30,000 (single)

1,00,000 (agg.) |

| 1025* | 194M | Payment by Indv./HUF (non-audit) to contractor / professional | 393(1)[Sl.6(ii)] | 2% | 50,000 |

| 1026 | 194J(a) | Technical Services; Royalty on films; Call centre operations | 393(1)[Sl.6(iii).D(a)] | 2% | 50,000 |

| 1027 | 194J(b) | Professional fees — Doctor / CA / Lawyer / Engineer / Architect | 393(1)[Sl.6(iii).D(b)] | 10% | 50,000 |

| 1028 | 194J(b) | Director remuneration / fees / commission (non-salary) | 393(1)[Sl.6(iii).D(b)] | 10% | — |

| 1032 | 194P | Specified Senior Citizen — bank TDS on total income | 393(1)[Sl.8(iii)] | Slab | — |

Property, VDA & Others

| Code |

Old Sec. |

Nature of Payment |

New Section (IT Act 2025) |

Rate |

Threshold (Rs.) |

| 1010* | 194IA | Property purchase — buyer deducts TDS on consideration | 393(1)[Sl.3(i)] | 1% | 50,00,000 |

| 1011 | 194IC | Monetary consideration under JDA (Joint Dev. Agreement) | 393(1)[Sl.3(ii)] | 10% | — |

| 1012 | 194LA | Compensation — compulsory acquisition of immovable property | 393(1)[Sl.3(iii)] | 10% | 5,00,000 |

| 1030 | 194DA | Life Insurance maturity sum — taxable portion (incl. bonus) | 393(1)[Sl.8(i)] | 2% | 1,00,000 |

| 1031 | 194Q | Purchase of Goods (specified buyer, turnover > Rs.10 cr) | 393(1)[Sl.8(ii)] | 0.1% | Excess of 50 Lakh |

| 1033 | 194R | Business / profession perquisite or benefit — in cash | 393(1)[Sl.8(iv)] | 10% | 20,000 |

| 1035 | 194O | E-Commerce: sale by participant through operator platform | 393(1)[Sl.8(v)] | 0.1% | 5,00,000 (Indv./HUF) |

| 1037 | 194S | VDA / Crypto transfer — other than Individual / HUF | 393(1)[Sl.8(vi)] | 1% | 10,000 |

| 1067 | 194T | Payment to partner — salary / commission / bonus / interest | 393(3)[Sl.7] | 10% | 20,000 |

Winnings & Cash Withdrawal

| Code |

Old Sec. |

Nature of Payment |

New Section (IT Act 2025) |

Rate |

Threshold (Rs.) |

| 1058 | 194B | Winnings from lottery / crossword / gambling / card game — cash | 393(3)[Sl.1] | 30% | 10,000 (per txn) |

| 1060 | 194BA | Winnings from online games | 393(3)[Sl.2] | 30% | — |

| 1062 | 194BB | Winnings from horse race (bookmaker / licensed person) | 393(3)[Sl.3] | 30% | 10,000 (per txn) |

| 1063 | 194G | Commission / prize on lottery tickets (distributor / stockist) | 393(3)[Sl.4] | 2% | 20,000 |

| 1064 | 194N | Cash withdrawal — deductee is co-operative society | 393(3)[Sl.5.D(a)] | 2% | 3,00,00,000 |

| 1065 | 194N | Cash withdrawal — other than co-operative society | 393(3)[Sl.5.D(b)] | 2% | 1,00,00,000 |

| 1066 | 194EE | NSS withdrawal — amount u/s 80CCA(2)(a) | 393(3)[Sl.6] | 10% | 2,500 |

Non-Resident Payments

| Code |

Old Sec. |

Nature of Payment |

New Section (IT Act 2025) |

Rate |

Threshold (Rs.) |

| 1039 | 195 | Non-resident sportsman / entertainer / sports association | 393(2)[Sl.1] | Treaty / Act | — |

| 1044 | 194LB | Interest from Infrastructure Debt Fund — NR / foreign company | 393(2)[Sl.5] | 5% | — |

| 1045 | 194LBA | Business Trust — distributed income [Sch.V Sl.3.B(a)] to NR | 393(2)[Sl.6.E(a)] | 5% | — |

| 1046 | 194LBA | Business Trust — distributed income [Sch.V Sl.3.B(b)] to NR | 393(2)[Sl.6.E(b)] | 5% / 10% | — |

| 1048 | 194LBB | AIF income to non-resident unit holder — non-exempt portion | 393(2)[Sl.8] | 10% / 30% | — |

| 1050 | 196A | MF / specified company units income — non-resident | 393(2)[Sl.10] | 20% | — |

| 1055 | 196D | Income from securities — Foreign Institutional Investor | 393(2)[Sl.15] | 20% | — |

| 1057 | 195 | Any interest / other sum chargeable — NR or foreign company | 393(2)[Sl.17] | Act / DTAA | — |

TCS — Tax Collected at Source

| Code |

Old Sec. |

Nature of Payment |

New Section (IT Act 2025) |

Rate |

Threshold (Rs.) |

| 1068 | 206C(1) | Sale of Alcoholic Liquor for human consumption | 394(1)[Sl.1] | 2% | — |

| 1069 | 206C(1) | Sale of Tendu Leaves | 394(1)[Sl.2] | 2% | — |

| 1070 | 206C(1) | Sale of Timber (forest lease / other) | 394(1)[Sl.3] | 2% | — |

| 1073 | 206C(1) | Sale of Scrap | 394(1)[Sl.4] | 2% | — |

| 1074 | 206C(1) | Sale of Minerals — coal, lignite or iron ore | 394(1)[Sl.5] | 2% | — |

| 1075 | 206C(1F) | Sale of Motor Vehicle — above prescribed threshold | 394(1)[Sl.6.D(a)] | 1% | 10 lakh |

| 1076 | NEW | Sale of Luxury Goods (watch, art, yacht, bag, shoes etc.) | 394(1)[Sl.6.D(b)] | 1% | Notified |

| 1086 | 206C(1G) | LRS — Education or Medical treatment (above threshold) | 394(1)[Sl.7.D(a)] | 2% | 10,00,000 |

| 1087 | 206C(1G) | LRS — Other purposes (above threshold) | 394(1)[Sl.7.D(b)] | 20% | 10,00,000 |

| 1088 | 206C(1G) | Overseas Tour Package — up to prescribed threshold | 394(1)[Sl.8.D(a)] | 2% | — |

| 1089 | 206C(1G) | Overseas Tour Package — above prescribed threshold | 394(1)[Sl.8.D(b)] | 2% | — |

| 1090 | 206C(1) | Use of Parking Lot / Toll Plaza / Mine or Quarry | 394(1)[Sl.9] | 2% | — |

For complete Non-Resident TDS, refer to Codes 1039–1057. For full TCS list, refer to Codes 1068–1092.

Source: Income Tax Act, 2025

For personalised advice on TDS compliance under the new Income Tax Act, 2025, contact Sompalli & Co., Chartered Accountants.